FP&A/Finance transformation practitioners in every sector need easier analytics. Whatever your business challenges, you need more insights and less manual work finding data. But in retail banking, this challenge is especially prevalent. Retail banks need to have efficient methodologies in place to forecast borrower accounts by cost center, build origination accounting treatments, load stock-based compensation via operating expense planning, and have an access-controlled centralized place to load and plan for new assets via capital expense planning. Simplifying analytics for this level of activity is difficult, especially when your organization is likely utilizing dozens of outdated overlapping disparate systems.

As with any enterprise systems design, having a modern data management strategy (inbound and outbound) is a prerequisite for any transformation. Banks will likely have multiple sources housing data:

- GL source for actuals

- HRIS source for headcount

- Lending source for loans

- Investment source for treasury/interest expense/cost of funds

- Banking source for deposit data

- Actuary source for credit losses/CECL provisions

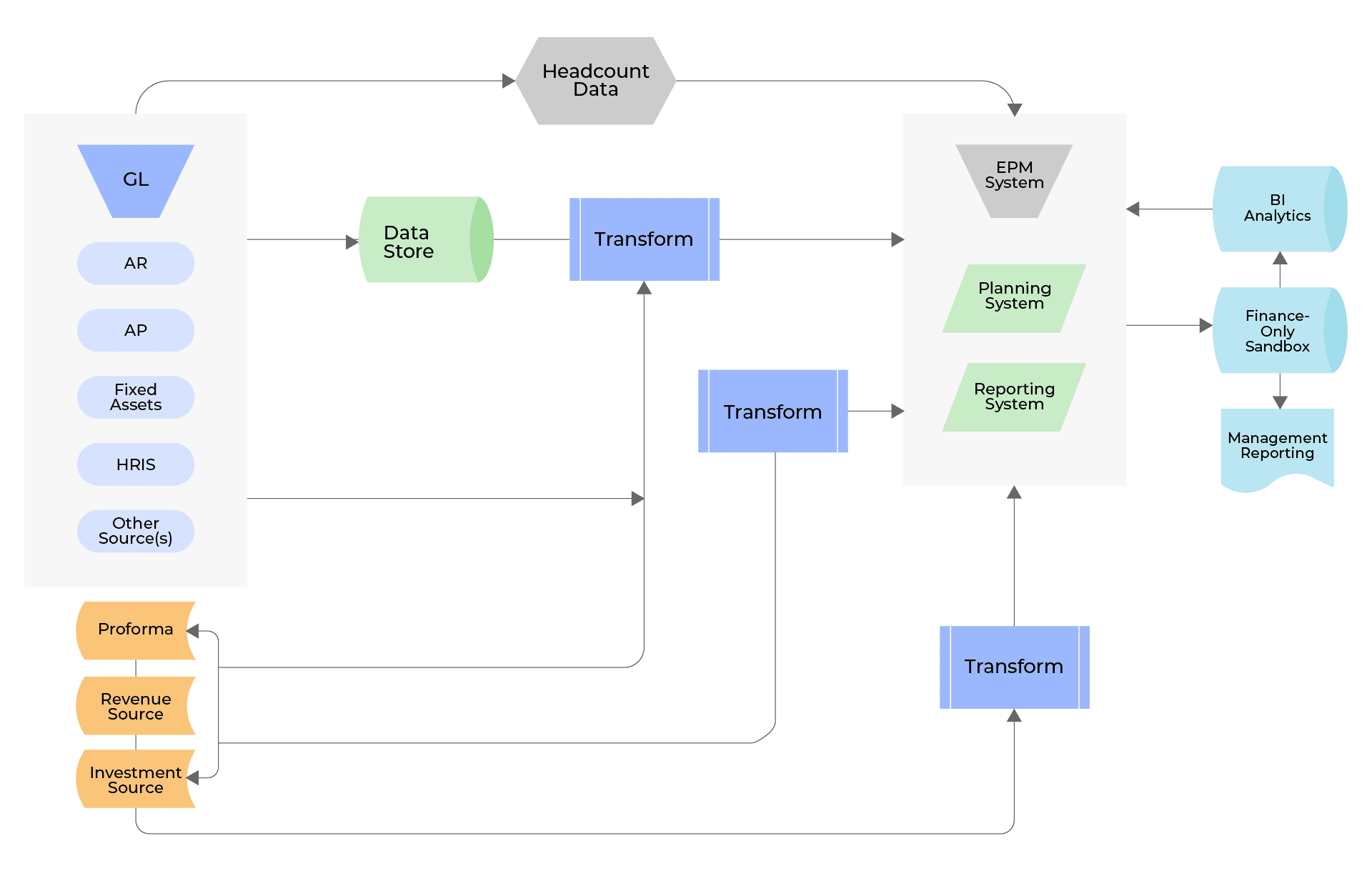

Here is an example of one retail bank’s architecture after nearly 30 years of “homegrown” evolution, and nearly 70 overlapping disparate systems:

If this system looks complicated, it should. The banking ecosystem is largely managed through legacy homegrown systems, often outdated and difficult to maintain, and highly disparate with many systems overlapping similar functionalities.

Retail Bank FP&A Transformation can be Easier

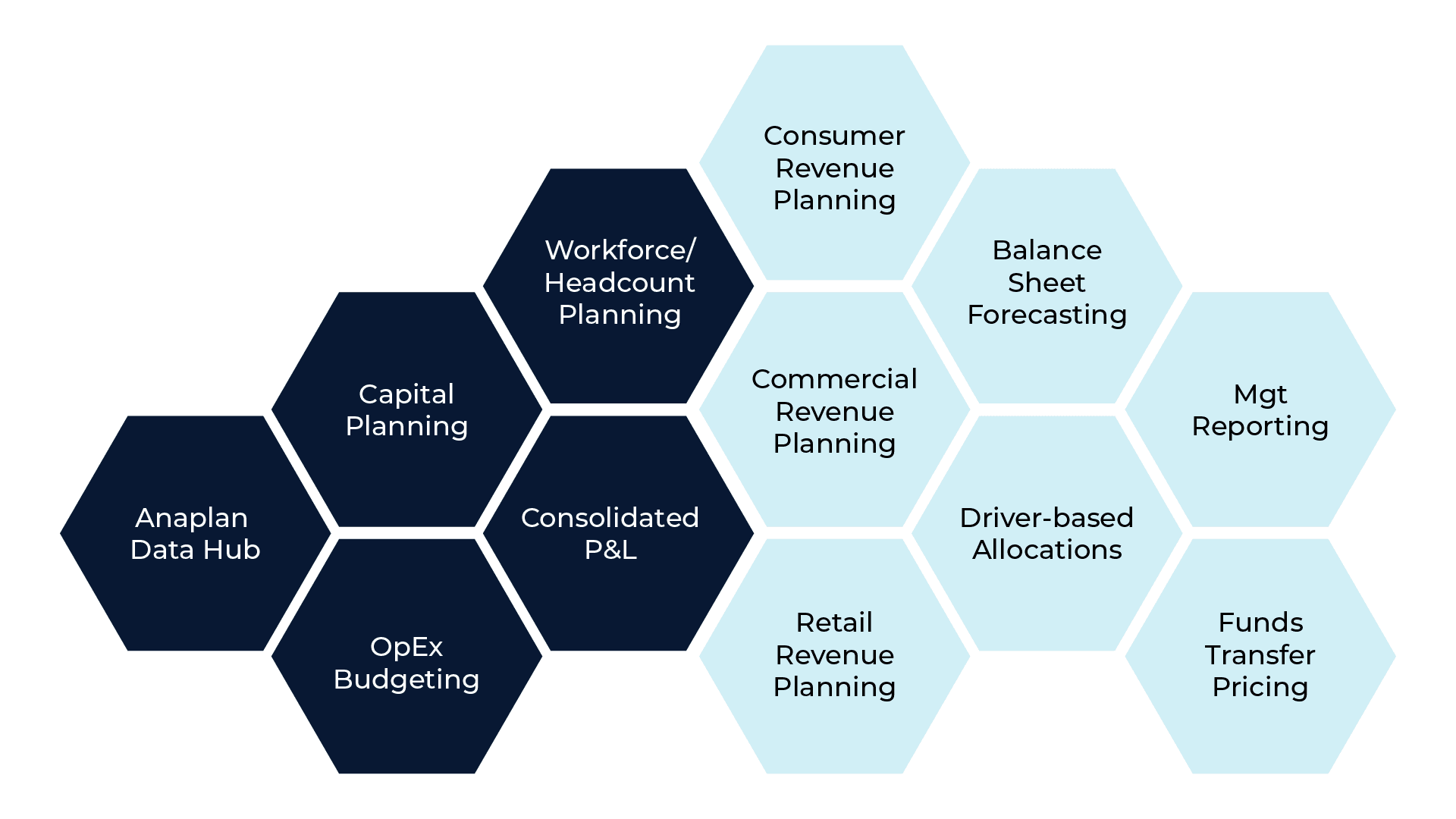

Modern banks understand that they need solutions for their planning, budgeting, and forecasting processes with significantly more flexible ad-hoc planning and scenario modeling capabilities. By automating, structuring, and connecting both financial and operational use cases, retail banks can understand and improve business performance across consumer and commercial revenue streams.

To achieve this, larger banks need more sticky “what-if” analysis capabilities and more self-service usability. FP&A transformation staff need to be able to quickly get to the data they want—for example, the ability to pull a detailed balance sheet capturing Holding Company vs. Bank vs. Consolidated views. Commercial banks also require lower-level insights into deposit and interest income modeling, product loans, and customer acquisition costs, as well as costs to maintain models.

This kind of approach simplifies things for retail banks—but with complex and outdated ecosystems as the starting point, many banks believe that enterprise system transformations will be long, expensive, and difficult to manage.

While such a FP&A transformation isn’t easy, it also doesn’t have to be a struggle. A templatized approach centered on best practices can relieve much of the burden of these types of transformations. Here are a few steps to consider before embarking on any transformation:

Not Every Implementation Needs to be a Full “Transformation”

The term “transformation” is often used as shorthand for any overhaul or replacement of an existing system. While the word does capture the positives of what you want—who wouldn’t want to transform a system that frustrates them every day? —it’s also a bit of a daunting term for a process that should make your life easier.

Even the biggest implementations are incremental. Think about your financial operations as a collection of smaller functions and consider how they fit together. As you plan your transformation, think about how you can phase your implementation according to your own bandwidth and priorities. Bring a few new capabilities in at the time, and keep working at it, and you’ll be in a better position in no time.

Start with the End in Mind

Having a clear vision for the end-state can be difficult. An implementation will likely be a long-term, multi-stage project, and creating the final plan takes strategic insight. Your planning process should start with high-level business goals and then establish the final architecture that will help you achieve these goals.

Big change can also create angst within the organization. This is frustrating to manage, but remember that this angst is primarily coming from individuals who are navigating imminent change. Again, think about how you can phase your implementation. With a step-by-step approach, change will happen in small doses over time, and your end users will see benefits early. If you achieve this, you’ll show your team that change isn’t scary, and you’ll get more people on board earlier. Which brings us to…

Identify Your Change Champions

Even before you begin your work, you’ll need champions who can help bring along the rest of your team. Without these champions, a six-figure project can easily turn into a seven-figure herculean lift. Find champions on teams that will be navigating the most change and use them early and often throughout the process. They can help in numerous ways: understanding system requirements, predicting where challenges will crop up, training end users, and acting as a sounding board. Pick a few champions early, selecting people with expertise and the trust of their colleagues, and bring more in as needed.

Choose the Right Partner

For many retail banks, just keeping systems running takes up most of your technical staff’s time. Actually managing the implementation is an even bigger challenge, and so most retail banks choose to bring in an implementation partner.

Of course, not all partners are created equal, and there’s no one measurement of the right partner for your retail bank. However, the right partner will have a few basic capabilities: the strategic lens to manage a multi-phased project, the industry specialization to tailor the solution for retail banks’ needs, and the technical expertise that focuses on quality. Remember, these programs often require onboarding team members as well, so measure your implementation partner’s change management capabilities. Finally, take your time: Choosing the right partner is an important decision, so measure twice and cut once.

For Retail Bank FP&A Teams, a Better System can be Your Competitive Advantage

As retail banks navigate a competitive ecosystem full of established players and new competitors, analysis will help you maintain an advantage. Keeping costs low and maintaining a profitable balance of services and products takes better insights than a legacy system can provide, so make sure your capabilities are ready.

Spaulding Ridge has built Anaplan implementations for companies across the financial sector, from helping them identify the capabilities they need to building their systems to assisting with change management and system acceptance. If you’re considering what your retail bank needs from its FP&A systems, please reach out to us!